Structuring your insurance: Stepped vs Level vs Blended Premium Back

Life insurance premium structure is very important because this can have a huge impact on the premium amount and Cash flow.

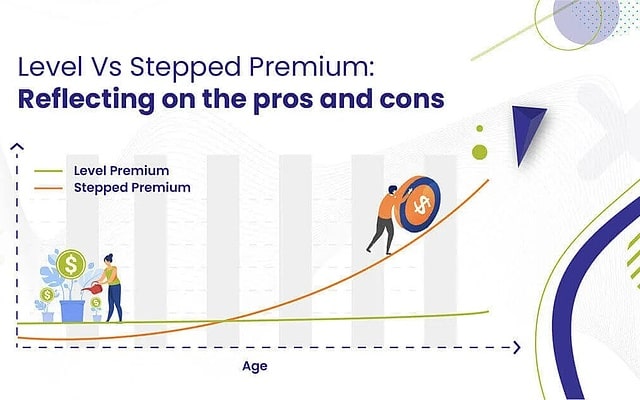

Stepped premiums:

Stepped premium structure is a type of premium structure in life insurance policies where the cost of the cover is recalculated each year based on the policyholder's age at the policy anniversary. This means that the premium will increase each year as the policyholder gets older. Stepped premiums may offer initial cost savings and may be suitable for short-term insurance needs. This type of premium structure will generally suit people who only want cover for 3 to 7 years or wanting to restructure the policy on regular intervals.

Level premiums:

Level premium structure in life insurance policies where the premium is spread more evenly over the life/tenure of the policy. Level premiums will generally be more expensive in compare to stepped premium Structure, but they provide lasting cost certainty. Under level premiums, the premium is calculated based on the age the policyholder was, at the time of policy enforcement, and it remains the same throughout the life of the policy.

Blended premiums:

This type of premium is a mixture of Stepped and Level premiums. The Insurance Policy goes from a higher-than-normal stepped style premium to a level style premium. Substantial premium savings are generated when compared to stepped over the long term. Sometimes an insurance policy can have a hybrid premium structure. This is often when an equivalent policy has both stepped and level premiums. For instance, you would possibly find a policy that has level premiums until you reach the age of 50 and then stepped premiums after that.

The distinction among three premium structures can be illustrated as under:

|

Age |

Stepped Premium |

Level Premium |

Optimum Premium |

|

42 |

$1,262.53 |

$4,992.82 |

$1,698.04 |

|

43 |

$1,447.87 |

$4,992.82 |

$1,852.35 |

|

44 |

$1,666.19 |

$4,992.82 |

$2,031.76 |

|

45 |

$1906.84 |

$4,992.82 |

$2,327.56 |

|

46 |

$2,126.08 |

$4,992.82 |

$2,597.07 |

|

47 |

$2,412.14 |

$4,992.82 |

$2,948.71 |

|

48 |

$2,777.66 |

$4,992.82 |

$3,398.04 |

|

49 |

$3,268.70 |

$4,992.82 |

$4,001.68 |

|

50 |

$3,735.72 |

$4,992.82 |

$4,575.74 |